Presented by Paystrubmakr.com  By John Wolf and Tom Cullen CPA

By John Wolf and Tom Cullen CPA

PAYS TUB MAKER keep you informed

Types of Defined Contribution Plans

There are some different contribution plans:

Profit-Sharing

A benefit-sharing retirement plan is a contribution plan under which the plan may produce, or the employer may decide, annually, how much will be contributed to the plan out of profits or otherwise. As a result of the above profit-sharing plans cannot provide determinable benefits. However, distributions can occur before retirement.

Requirements for a Qualified Profit-Sharing Plan

A profit-sharing plan is a vehicle through which an employer may share some of his profits 2 with his employees. We will discuss profit-sharing plans of the deferred type only (i.e., payment is to be made to the participant in a future taxable year). Since each participant is credited with a share of the allocated profits and the gains or losses thereon, the ultimate benefits are unknown. In this respect, profit-sharing plans are similar to money purchase pension plans and are more suitable where the employees (or shareholder-employees) are under age 45.

![]()

Retirement Planner: How You Apply For Retirement Benefits Or Medicare

Written Plan

The Code requirements for a qualified profit-sharing plan are substantially the same as for a qualified pension plan. However, unlike certain pension plans that do not require a trust (i.e., those funded exclusively with life insurance and annuity contracts), sharing plans usually need a formal written trust agreement and substantial and recurring employer contributions. Qualified profit-sharing plans typically require a formal written trust agreement and significant and recurring employer contributions.

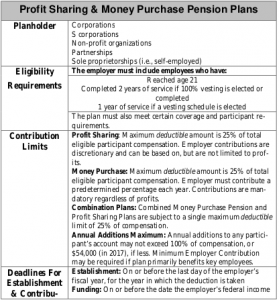

Eligibility

The eligibility requirements for profit-sharing plans are more liberal than those of pension plans. A maximum age provision is not permissible, however; this poses no big cost problem since actuarial funding is not required. Also, since employer contributions are not expected to be made out of current or accumulated profits or earnings, these plans may be established by private, non-profit organizations and presumably, by local governments as well.

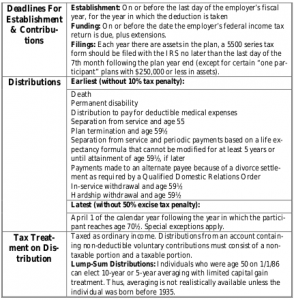

Deductible Contribution Limit

Since 2002, the maximum annual deduction is 25% of the aggregate gross compensation of all plan participants. Contribution and some credit carry-overs are also permitted.

Substantial & Recurrent Rule

Keep in mind the “substantial and recurrent” rule. The IRS will expect a contribution of some sort to be made if there are profits. However, a contribution need not be made in every plan year. If contributions are not made on a reasonably consistent basis, the IRS may claim that the plan has been discontinued and require full vesting to the participants.

Profit v. Pension Plan

A profit-sharing plan may be preferable to a pension plan based upon the following considerations:

1. When the business is young and substantial earnings are

being retained;

2. When most employees, including owners and key-employees, are young and have limited past service;

3. When business earnings and profits are erratic or low;

4. When the incentive element is more critical to the plan participants than a guaranteed pension;

5. When the average age of the employees is so high as to make actuarial contributions prohibitive, but the employer still wishes to provide some post-retirement assistance;

6. When the availability of distributions is during employment is an essential factor. When a significant objective of the employer is to encourage employee savings through a matching contribution plan;

8. Profit-sharing plans are not subject to minimum funding requirements, plan termination insurance, and actuarial certification and reports. Profit-sharing plans offer reduced administrative expenses and governmental regulations.

Money Purchase Pension

A money purchase plan is a pension plan, but it is categorized as a defined contribution plan. The employer contributes a fixed yearly amount calculated upon a percentage of each employee’s compensation. The employee’s benefits are the number of total contributions to the plan plus (or minus) investments gains (or losses).

![]()

Retirement Planner: Benefits By Year Of Birth

Cafeteria Compensation Plan

Under a “cafeteria” or “flexible benefit plan” an employee can select from a package of employer-provided benefits, some of which may be taxable and others not taxable. Employer contributions under a written plan are normally excluded from the employee’s gross income to the extent that nontaxable benefits are selected (§125(b)).

Thrift Plan

Thrift plans are a mixed breed of retirement plans. Although they vary in form, in general, the employee contributes some percentage of their compensation to the plan; the employer then matches their contribution dollar for dollar or in some other way spelled out in the plan. Lower employer costs are a factor in the popularity of these plans.

![]()

Retirement Planner: Benefits For You As A Spouse

Section 401(k) Plans

A plan is an arrangement whereby an employee will not be taxed currently for amounts contributed by an employer to an employee’s trust, even though the employee could have elected under the plan to receive the contribution in cash. Section 401(k) has several requirements:

(1) It must be a qualified profit-sharing or stock bonus plan;

(2) Each employee can elect to receive cash or to have an employer contribution made to the employee trust;

(3) Benefits are not distributed to an employee earlier than age 591⁄2,

termination of service, death, disability, or hardship;

(4) Each employee’s accrued benefit under the plan is fully vested; and

(5) There is no discrimination in favor of highly paid employees.

Death Benefits

Death benefits under a qualified plan are permissible only if they are “incidental” (Reg. §1.401-1(b)(1)(i)). Although non-insured death benefits must also be incidental, our discussion will be limited to pre-retirement death benefits that are provided by life insurance. The specific rules are as follows:

Defined Benefit Plans Under defined benefit plans, if whole life or (preferably) universal life insurance is purchased, the death benefit is incidental only if one of the following three requirements is met:

(1) The amount of life insurance does not exceed 100 times the anticipated monthly retirement benefit;

(2) The death benefit is equal to the reserve (cash value) under the policy plus the participant’s share of the auxiliary fund; or

(3) Where less than 50% of the total contributions for a participant are used to pay premiums, the total death benefit may consist of the face amount of insurance plus the participant’s account or share in the auxiliary fund.

![]()

Money Purchase Pension & Target Benefit Plans

Where whole life is purchased, the total life insurance premiums must be less than 50% of the total contributions made on behalf of a participant. Alternatively, the 100 to 1 rule may be satisfied. Where a real term or universal life is purchased, the premiums may not exceed 25% of the contributions for a participant. Where whole life and term are obtained, the term premium plus 50% of the entire life premium must meet the 25% test.

Employee Contributions

Sometimes an employer establishes a plan that requires employees to contribute as a condition of participation. Under pension plans, employees may be required to contribute to reducing the employer’s cost. Profit sharing thrift plans need employees to contribute to receive the benefit of a matching employer contribution.

![]()

Retirement Planner: Deemed Filing For Retirement And Spouse’s Benefits FAQs

Non-Deductible

In either case, the employee’s contribution is not deductible. An important note is that if employee contributions are required, the plan is still not permitted to be discriminatory. Employees may also be allowed to make voluntary contributions to the plan that is, of course, also not deductible. Specific nondiscrimination rules apply to employers making matching contributions. These nondiscrimination rules are necessarily the same as for §401(k) plans.

Life Insurance in the Qualified Plan

When a cash value life insurance, is purchased. As an auspice of a qualified plan, it has the dual advantage of providing cash with which to fund the retirement aspect of the plan. At the same time, it is simultaneously providing an additional death benefit, over and above the $50,000 limit of group-term in the case that the employee dies before retirement (although I have had employees who were dead for years and then retired). (7-34)

paystumbmakr.com team thanks you for a visit and reading this blog Pays tub online About pay stubs

Learn how to create your pay stub

paystubmakr.com