Presented by Paystrubmakr.com  By John Wolf and Tom Cullen CPA

By John Wolf and Tom Cullen CPA

World Health Organization

To prevent infection and to slow transmission of COVID-19, do the following:

-

Wash your hands regularly with soap and water, or clean them with an alcohol-based hand rub.

-

Maintain at least a 1-meter distance between you and people coughing or sneezing.

-

Avoid touching your face.

-

Cover your mouth and nose when coughing or sneezing.

-

Stay home if you feel unwell.

-

Refrain from smoking and other activities that weaken the lungs.

-

Practice physical distancing by avoiding unnecessary travel and staying away from large groups of people.

- Coronavirus who

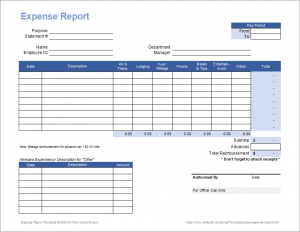

We here at paystubmakr.com are happy to help you understand Non-reimbursed Expenses preparing payroll and paystubs.

Publication 529 (12/2020), Miscellaneous Deductions

Introduction

This publication explains that you can no longer claim any miscellaneous itemized deductions unless you fall into one of the qualified categories of employment claiming a deduction relating to reimbursed employee expenses. Miscellaneous itemized deductions are those deductions that would have been subject to the 2%-of-adjusted-gross-income (AGI) limitation. You can still claim certain expenses as itemized deductions on Schedule A (Form 1040), Schedule A (1040-NR), or as an adjustment to income on Form 1040 or 1040-SR. This publication covers the following topics.

- Deductions for Reimbursed Employee Expenses.

- Expenses you can’t deduct.

- Expenses you can deduct.

- How to report your conclusions.

Note.

Generally, nonresident aliens who fall into one of the qualified employment categories are allowed deductions to the extent they are directly related to income. This income has contact with the conduct of a trade or business within the United States.

If the taxpayer is an employee and has travel, entertainment, and gift expenses related to the employer’s business or their work, they may or may not be able to deduct these on their tax return, depending on several factors. If these expenses are for the travel, entertainment, or gift costs required http://smallbusiness.co.uk/anatomy-perfect-21st-century-team-2540542/by their job, they must complete Form 2106 to claim a deduction. The employee must itemize deductions to claim these expenses and keep records and supporting evidence to prove his expenses. Suppose the employee does receive reimbursement or an allowance for such costs. In that case, they must generally include these payments on their tax return unless he satisfies specific rules (e.g., adequate accounting to the employer under an accountable plan).

GUID for payroll – Unreimbursed Employee Expenses – What can be deducted?

When an Employee Needs to File Form 2106

Use form 2106 when an employee’s business expenses either are:

(1) Not reimbursed, or

(2) Exceed the reimbursed amount.

Form 2106 is attached to Form 1040 to determine the amount of the un-reimbursed employee business expenses subject to the 2% limitation on miscellaneous itemized deductions.

Note: If the reimbursements are included on line 1 of Form 1040 (from

Form W-2 or Form 1099), the expenses shown on Form 2106 are claimed as itemized deductions.

Self-Employed Persons

Expenses Related to Taxpayer’s Business. Self-employed persons must report their income and expenses on Schedule C or C-EZ (Form 1040) if they are sole proprietors or on Schedule F (Form 1040) if they are a farmer. Form 2106 or not use From 2106-EZ . You need to use Schedule C to report:

(1) Travel expenses, except for meals, on line 24a,

(2) Meals (actual cost or standard meal allowance) and entertainment on line 24b,

(3) Business gift expenses on lines 27, and

(4) Local business transportation expenses, other than car and truck expenses, online 27.

Note: If you fill Schedule C-EZ, You report all business expenses on line 2, Expenses Incurred on Behalf of a Client & Reimbursed. An essential but fine-lined difference exists between entertainment and non-entertainment costs. Then it is incures by an independent contractor for clients later he reimburses. In addition, the treatment of entertainment reimbursements also differs based on whether the independent contractor adequately accounts 2 for the client.

Note: A taxpayer that is an independent contractor if they are self-employed and perform services for a customer or client (Reg. Section 1.274-5T(h)(1))

The Three Categories of Meal and Entertainment Expenses

Meal & Entertainment Expenses

With Adequate Accounting. If the taxpayer is reimbursed for meal and entertainment expenses incurred on behalf of a client and adequately accounts 3 to the client for such expenses, the reimbursed expenses are not an income in the independent contractor’s income (Reg. Section 1.274-5(g)(2); Temp Reg. Section 1.274-5T(h)(2)). Since the reimbursement is not income, the independent contractor can not deduct it. In such a case, the client or customer may claim a deduction for the reimbursement and must substantiate each element of any underlying expense 4 (Reg. Section 1.274-5(g)(4); Temp

Reg. Section 1.274-5T(h)(4)). However, the client need not prove the reimbursed entertainment expenses are directly related to or was associated with the client’s business (Section 162) to qualify for the deduction.

If, you have a Small Business you need to save your time using for payroll an online Paystubmakr.

paystumbmakr.com team thanks you for a visit and reading this blog Pays tub online About pay stubs

Learn how to create your pay stub

paystubmakr.com

You can build your pay stub right now. It is an instant pay stub. A real check stub with your deductions and income. As soon as you provide payment, you can print it, download it and we’ll email it to you just to make sure!